Engage

12 min read

12 min readUsing data to understand open banking opportunities

The open banking data economy is expanding at a rapid pace, where a customer's data can be used (with their consent) to provide better financial services and digital products, including across an embedded finance customer journey. But data can also be used by stakeholders to better understand the open banking, open finance and embedded finance ecosystems and the emerging opportunities and challenges when designing new services, entering new markets, building partnerships and complying with regulation.

Five current trends demonstrate how valuable data is becoming for strategic decision-making by stakeholders within the open banking and related ecosystems:

- Ecosystem thinking

- Regulatory advancements

- Stakeholder relationships

- Investment pivots

- Acquisition headwinds.

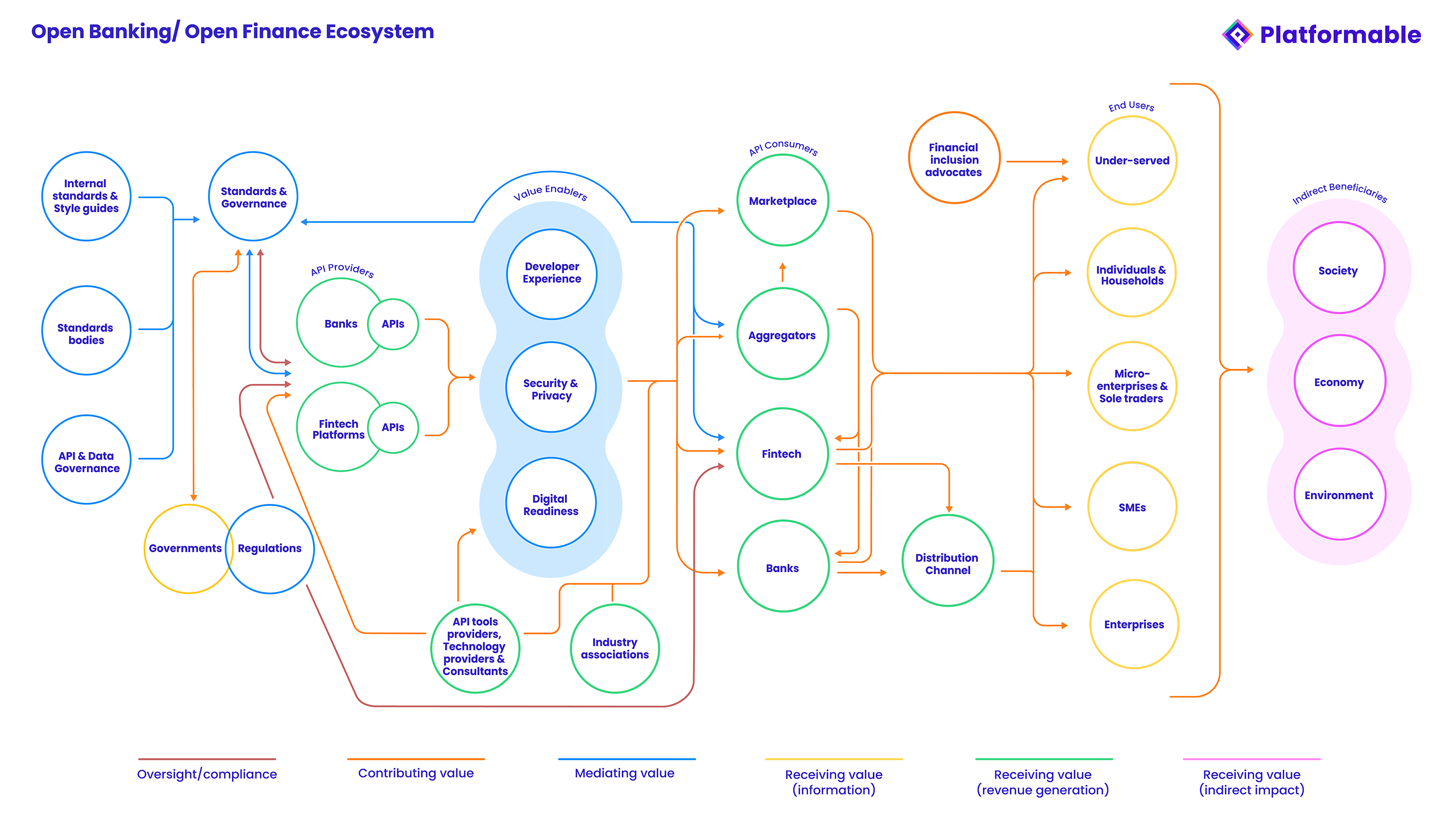

When I started Platformable, I knew that there would be a growing need to understand key components of the open banking ecosystem as it evolved. As a team, we created an ecosystem model that identifies how value is generated and distributed across open banking amongst all stakeholders, and what components we saw as essential to the efficient and effective functioning of the ecosystem. From that, we then identified the datasets that we thought would help analyse open ecosystems.

Our data has since been used by payments providers, aggregators, banks, fintech, industry associations, regulators, and leading academics and research teams around the globe, and we are excited to make this data even more readily accessible through our trends reports and dashboard products.

Since the start of the year, we have been tracking the growing interest in the value of data to aid in strategic decision-making amongst open banking stakeholders and have identified 5 trends.

Ecosystem thinking

While at Platformable we have been talking about the value of ecosystem-based approaches (and redesigned our website to include a resource hub — our "Understand" section), the wider open banking and related sectors have only more recently begun to explore what this means. For several years, as we released open banking trends data, we described how banks and fintech providers could move to platform-based business models, and/or choose to become the underlying infrastructure for others in a Banking-as-a-Service (BaaS)-model approach (a specific type of platform play).

When we talked about platforms in this way, we described how that would then lead to an ecosystem around the platform: partners and third parties building new products and services that drew on the APIs being made available by the bank or fintech platform provider. We also talked about open banking in a wider ecosystem context: the whole open banking sector itself is an open ecosystem (that is, a network of equitable participation opportunities that allow stakeholders to co-create, collaborate, complement, and/or compete with each other by using common tools (APIs), open source, and infrastructures).

We developed a model to describe and show this which includes the role of standards bodies, API providers, industry associations, and essential ecosystem enabling non-stakeholder components like regulations, data governance approaches, security, digital readiness, and so on:

Recently, we have seen an increase in the sector recognising and discussing this shift towards ecosystems:

- Industry association Mobey Forum's recent member event in Barcelona, in which I gave a keynote, focused on payments ecosystems

- Banks like Standard Chartered are expanding their open banking APIs and developer portal with a greater focus on acknowledging ecosystem-driven approaches

- Analysts and service providers are reframing their narratives to describe a burgeoning ecosystem: Analyst firm Bankinghub in Europe and aggregator platform Plaid's blog posts recently both shifted focus to describe the open banking sector as an ecosystem

- World Bank's CGAP Initiative (where I provided services years ago on API governance before it was widely recognised as an issue and on the potential of APIs for creating financially inclusive products) is now shifting to describing open finance ecosystems rather than describing APIs directly.

To better understand how ecosystems are playing out, data will be needed to map the stakeholders, enabling environment, and relationships between stakeholders.

Regulatory advancements

Emerging regulations that further advance open banking, open finance and embedded finance point to the increased importance of ecosystem approaches. New European Digital Identity regulations are a good example. This new regulation, expected to commence in 2025 but rolled out over subsequent years, elevates the importance of identity providers in the wider ecosystem.

We believe identity will play a huge role in how banks and fintech platforms engage in the emerging embedded finance sector. In embedded finance, the shift moves from transactional relationships with customers to supporting customers across their user journey. For example, it is less about buying a house than working with a customer across the house purchasing process: from selecting a home, applying for a mortgage, moving in and arranging insurance. Identity becomes the connector piece that allows banks or fintech services to maintain the relationship with a customer as they move from one stage to the next across that journey1.

In the same way that in Europe, the messiness of the less-opinionated Second Payments Services Directive (PSD2) allowed banks to create their own APIs which in turn led to a new ecosystem stakeholder in the form of API aggregators, here, regulations are playing a role in supporting identity providers and possible wallet holder services to take a more active ecosystem role, although in a more standardised way than we saw in PSD2.

Fintech, banks and other stakeholders need up to date data to understand the emerging regulatory environment and to start planning for new business models, relationship opportunities and compliance requirements well ahead of implementation. Data on emerging regulations and regulatory milestones also helps stakeholders participate more actively in policy development and consultation processes.

Stakeholder relationships

The range of stakeholders in the open banking ecosystem is growing and they are maturing at a faster rate. In recent years, API security providers have increased their ecosystem role, for example, by supporting banks and fintech to strengthen the resilience of their infrastructure. We map API tool ecosystem growth, and #% of all API pureplay security providers have a page targeting the banking and financial sector.

More banks have also shifted towards a platform mindset in which they are becoming (slightly) less paranoid about "owning the customer relationship" and are building partnerships and relationships with fintech. Some banks are also seeing opportunities in outsourcing innovation to their fintech partners, recognising their internal legacy systems and risk-averse culture is ill suited to testing new products and features with customers, allowing fintech to take on those roles at arms length.

In an ecosystem, there are also more complex relationships than in a traditional market. In the US and Nigeria, for example, competitors work together in standards bodies like FDX and Open Banking Nigeria to coordinate around new standards and data models for the sector. At other times, banks and fintech are collaborating or co-creating to bring new products and services to market. And at other times banks are competing directly. A bank may have multiple relationships in play with other ecosystem stakeholders, so data becomes important in understanding which role is relevant at what time, which data and strategies to share, and what elements should be treated as commercial-in-confidence at any given time. Drawing on ecosystem literature, we have mapped five types of relationships that we observe in open ecosystems.

When participating in open ecosystems, data is needed to understand when a fintech or bank should play a particular role, and what to share and what to treat as commercial-in-confidence.

| Relationship type | Co-create | Collaborate | Complement | Compete | Coordinate |

|---|---|---|---|---|---|

| Icon |  |  |  |  |  |

| Definition | The use of data, open APIs, and other digital components that allow consumers to build their own value. | When two or more entities identify a customer experience or product that they can deliver together, utilizing their respective core competencies. When this joint venture approach works most effectively, the value from the resulting solution is greater than the sum of its parts. The organizations involved form a symbiotic relationship: the offering creates a mutual dependency, but also offers mutual benefit. | When APIs are used to create additional value to a customer or user base. | When stakeholders directly compete with each other, for example, by offering APIs with the same functionalities to API consumers, or when two or more API consumers build products with similar value propositions for use by end customers. | Some ecosystem stakeholders may participate in an open ecosystem from a regulatory, standards or data intermediary perspective. These stakeholders may ensure stakeholders are participating to agreed legislative and regulatory constraints, may participate in order to assist with setting common standards and data models, or may manage ‘sandboxes’ and other test environments that allow other stakeholders to share data or services within a constrained setting in order to test proof of concepts. |

Investment pivots

Over the past two years, VC investment in fintech slowed down. At the same time, and not so coincidentally, the prevailing buzz that fintech are industry-wide disruptors coming to take the bank's lunch has also waned. While there have been some market-wide disruptors (Stripe, Adyen, Wise, Klarna, and so on), the true role of fintech in the open banking landscape has been reframed to be one of a more partner/collaborator model whose services are provided alongside banks, within bank ecosystems, or as a funnel to recruit new customers to banks. Part of this has emerged naturally, and partly because the initial wave of VC-investment hyped up encouraging fintech to scale to millions of customers as soon as possible (starting with demonstrating there was a global million/billion+ consumer market) rather than starting with a clear target market and growing from there — we have been discussing this at keynotes for over four years now).

As a result, fintech spent a couple of years in either two modes: chasing an enterprise customer that they could then use to demonstrate market fit and sell to all of their first customer's competitors as well; or focusing on building a generic, mass market, lowest-common-denominator product that didn't truly differentiate from the commoditised banking products that are already on offer (but perhaps with a better looking digital design).

Now with VC funding harder to gain, fintech and other stakeholders desperately need data to identify viable target segments, potential partners to work with, market context and regulatory understanding, business price modelling and competitor analysis, and so on.

Acquisition headwinds

A recent acquisition also points to how valuable data on open banking, open finance and embedded finance is becoming. Innopay was bought by Oliver Wyman.

While Innopay has a network of payments consultants and advisory services, their Open Banking Monitor shares data on a select range of banks, mostly in Europe, on a quarterly basis. While not as comprehensive as our dataset which tracks all open banking activity globally and includes over 2800 banks and close to 6000 API-ready fintech, Innopay's data is commendable and has served the consultancy group well when leveraging their payments experience to move into open banking consultancy projects. Oliver Wyman, a global consultancy group, no doubt purchased Innopay in part for their data as well as their growing open banking expertise, as well as to cement their footprint in Europe.

(Interestingly, some of our major clients have told us they chose us because, in their words, we are not "Oliver Wyman or Accenture or a large consultancy shop": We are seen as more flexible, data-focused, and as global experts on open banking trends which has enabled us to stay close to our customers rather than pass off new projects onto interns or junior staff who reiterate some of the common themes in open banking without understanding the data from an ecosystem perspective nor what it signifies in terms of emerging trends.)

Smart, scale-up businesses with an eye to consolidating their positioning in the open banking space are seeking to lock down access to open banking specific datasets to help them in marketing opportunities and to plan strategically. This is occurring as a range of market researchers calculate the global opportunity of open banking and related sectors:

| Forecast value | $36.3 billion | $11.7 billion | $11.7 billion |

|---|---|---|---|

| Discussion | "Europe’s embedded banking market is expected to reach a valuation of US$ 36,377.9 million by 2033." | "The Open Banking Solutions Market size is expected to grow from USD 5.5 billion in 2023 to USD 11.7 billion by 2028" | "The market for embedded finance is forecast to grow by 148% over the next five years... Juniper Research predicts that embedded finance revenue will exceed $228bn by 2028" |

| Source | https://www.fmiblog.com/2023/11/16/europe-embedded-finance-market-surges-with-robust-growth-envisions-a-remarkable-us-94081-7-million-by-2033-driven-by-a-solid-14-5-cagr/ | https://www.marketsandmarkets.com/Market-Reports/open-banking-solutions-market-160940134.html | https://www.finextra.com/newsarticle/43922/embedded-finance-market-to-be-worth-22bn-by-2028 |

Data is essential in an ecosystem mindset

Moving to an ecosystem mindset and understanding the various enabling components, relationships, gaps and opportunities in open banking means stakeholders will need greater access to well collected, methodologically sound datasets focused specifically on open banking, open finance, and embedded finance. Recent moves demonstrate this battle for access to ecosystem data is just heating up.

Contact Platformable to discuss accessing our open banking datasets, either directly or through our trends reports and dashboard product.

Article references

We see the same shift in open health ecosystems: traditionally, healthcare financing occurs at the point of acute service delivery, such as a surgery, but with an ageing population and growing healthcare costs, and the potential impact of new medications and therapeutic devices, changing healthcare financing to support patients to avoid hospital admission by managing their chronic illness or prevent negative health impacts means looking at a patient’s clinical care pathway from prevention to diagnosis to management to health intervention and involving ecosystem stakeholders at relevant points across this type of 'user journey.'

Mark Boyd

DIRECTORmark@platformable.com