Understand

16 min read

16 min readThe API Landscape: Measuring the Value Generated by API Tools and Consultants as Ecosystem Enablers

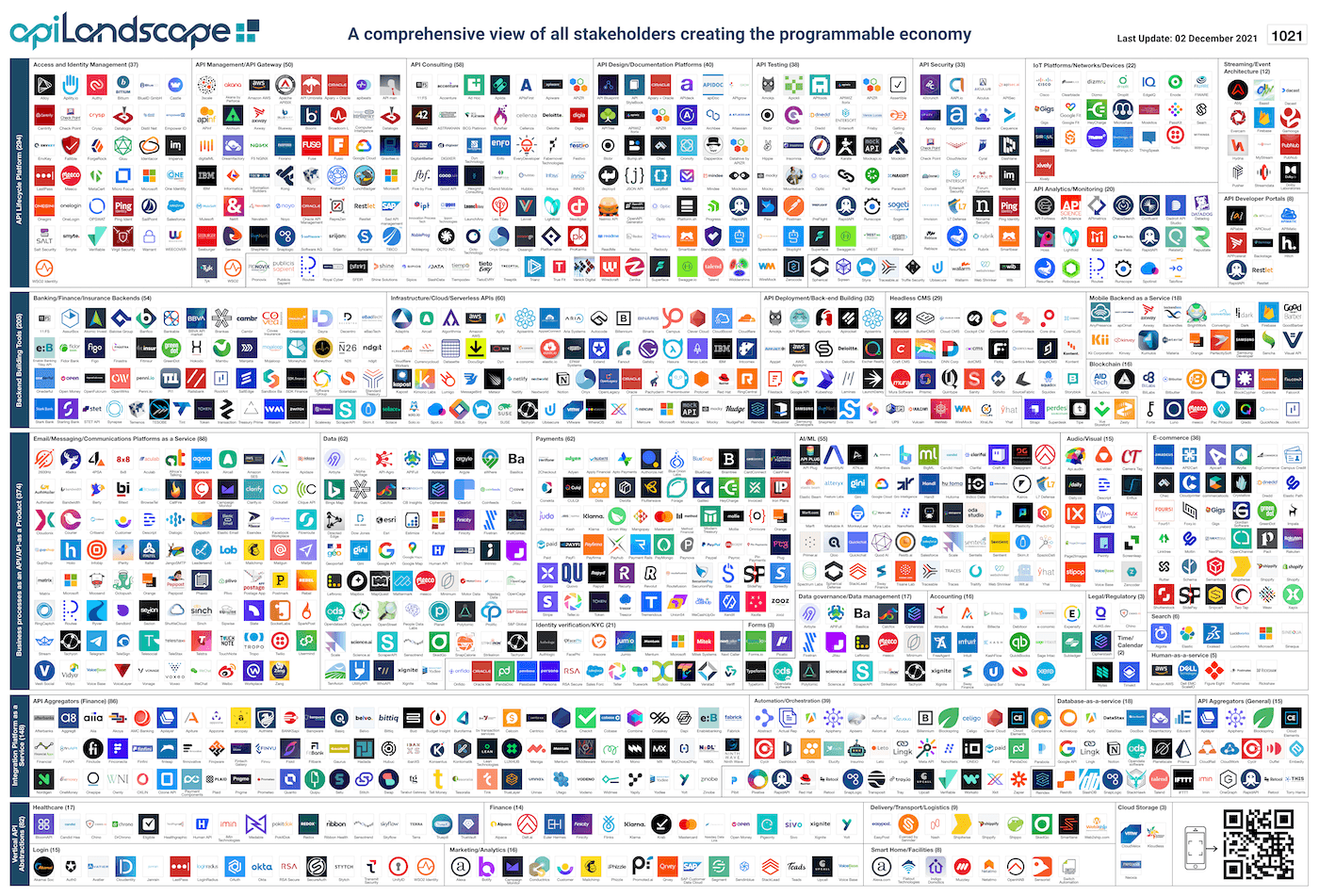

The apidays API Landscape Tool

At the global industry conference apidays Paris in December 2021, the industry community hub apidays released their latest API landscape, collecting over 1,000 API tools, open source projects and providers in one ecosystem map.

Platformable supported apidays to build their latest interactive tool. In previous years, apidays had created a static industry landscape map, but was looking to industry examples like the CNCF’s interactive Landscape and wanted to move to something similar.

Given our core business is creating ecosystem taxonomies and data models, building datasets, and measuring impact, this project was a great opportunity to work with a global leader in the API industry.

API tools providers and consultants are ecosystem enablers

API tools providers support digital businesses and organisations to implement API-first approaches, and provide the tools, open source technologies, products, services, and best practices to transform towards enabling an ecosystem of relationships to emerge.

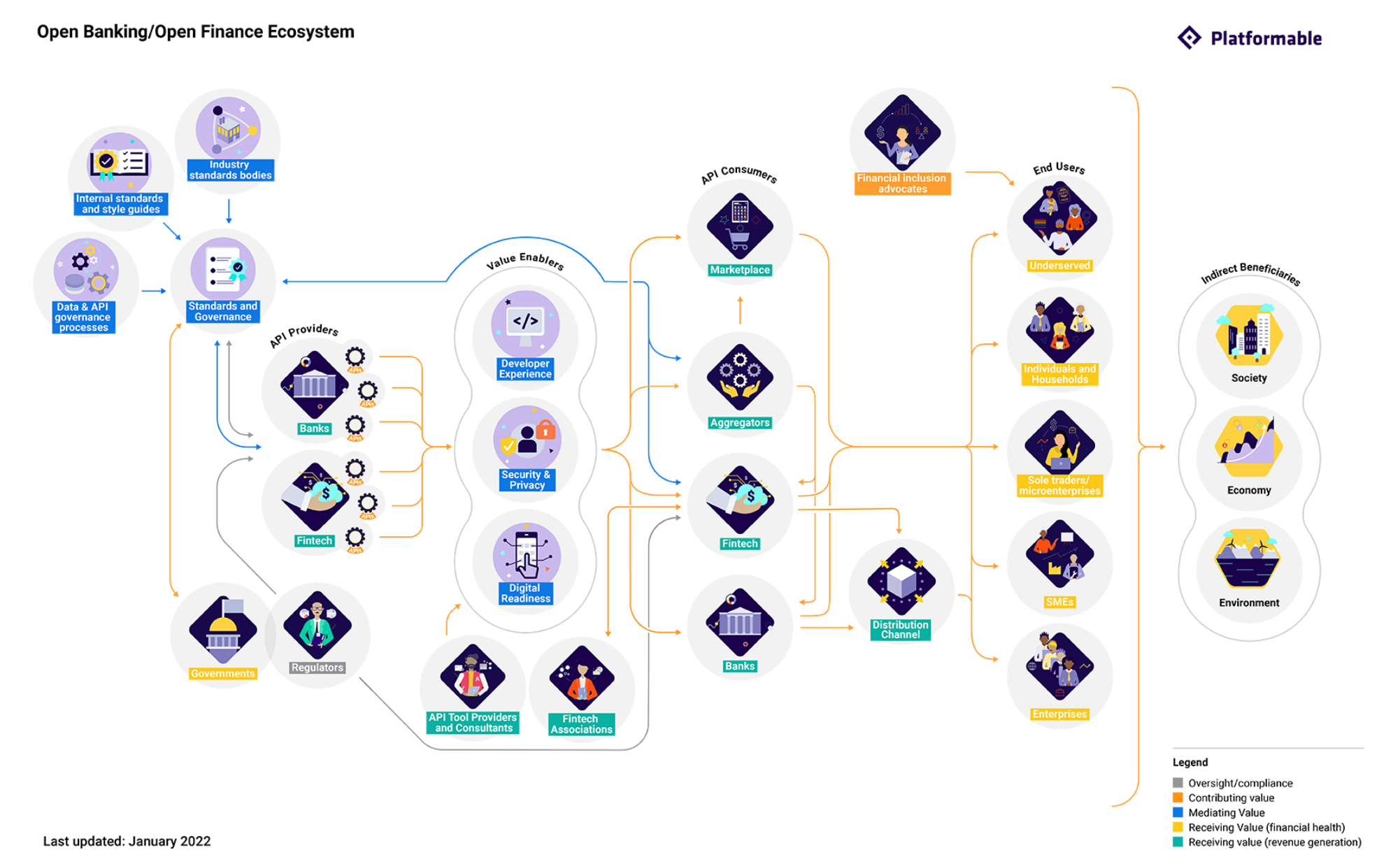

At Platformable, we have mapped the role that API tools and consultants provide in open ecosystems. For example, in open banking and open finance ecosystems, API tools and consultants support bank and finance platforms to provide APIs to API consumers (often fintech apps building with bank and payment APIs). The quality of those APIs, the developer experience in using them, the performance of the APIs, and the security and privacy controls of such tools will either limit or expand the size of the overall open finance ecosystem. With the help of API tools and consultants, API providers across banks and finance can increase the value that API consumers get out of using their APIs to build products and create automated workflows, which leads to greater adoption by end users. This generates revenue for both the API consumer fintech builders and to the banks and finance platforms that offer the APIs in the first place. We describe this in detail in our open banking/open finance ecosystem value model:

API tools providers and consultants facilitate open ecosystems because:

- They provide the technological infrastructure and tooling to make digital platforms possible

- They embed best practices in building and managing APIs into their product features

- They share case studies and metrics on what value is generated by their customers/users and others in their stakeholder ecosystem.

There are countless industry examples:

- API management platforms like Axway, Gravitee, and Sensedia enable banking, energy, health, education, and governments to move towards digital infrastructures and work with external partners to speed up product development, extend digital service choice, and make greater use of data for productivity.

- Analytics tools like APIMetrics enables digital businesses to measure the performance of the APIs they use. This is essential in sectors like finance where APIs must be able to access account information, and make instant payments securely.

- API security tools like 42Crunch and Traceable AI ensure that digital ecosystems are trustworthy and reliable for exchange of finances, sensitive data, and business transactions via APIs

- Regulatory and legal tech like ALIAS enable digital organisations to leverage APIs to ensure ongoing compliance that meets complex global data privacy and protection regulations

- API product providers like OpenCage, Clearbit and Twilio enable specific functionalities like geolocation, business information and contacts, and communication services to be embedded into a digital business’ workflows and products.

How we built the tool

Key findings from the API Industry State of the Market Report

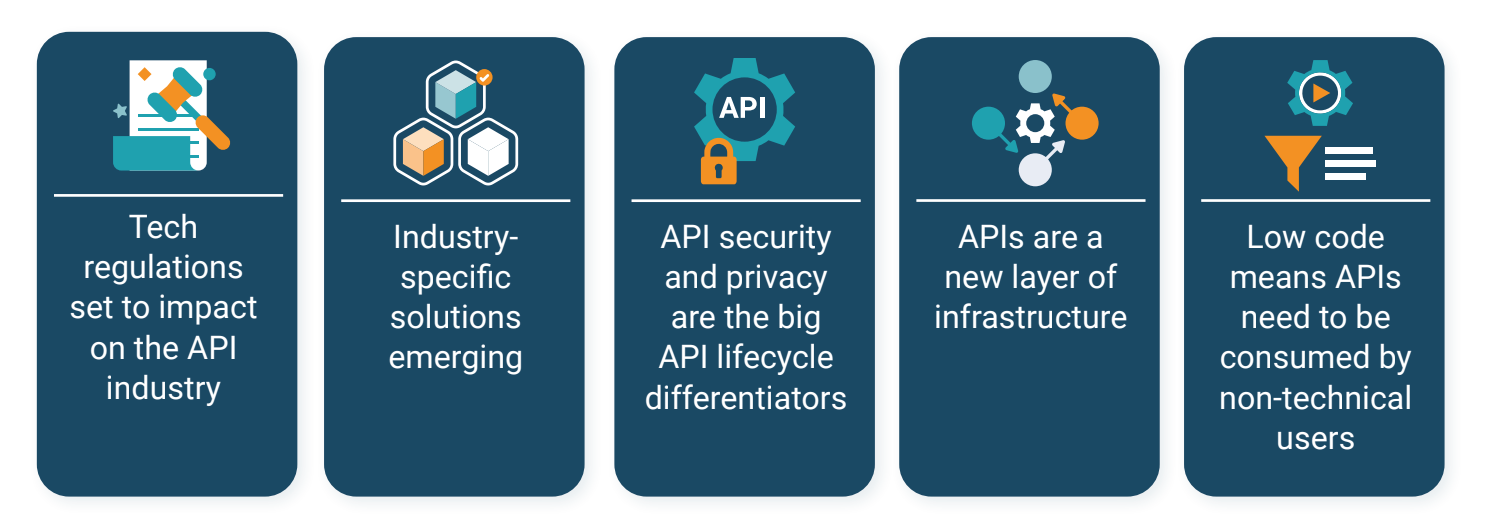

Analysing the data collected for the API Landscape, Platformable was also asked to work with apidays Founder Mehdi Medjaoui on unpacking the key trends we could see from the data and from our many conversations with API industry leaders and clients throughout the past year. Our API Industry State of the Market Report for 2022 identified five key trends:

- The explosion of tech regulations will impact the API industry: The API industry will need to be able to map regulatory impacts on their feature set and on their customer needs as global and local tech and data regulations increase.

- Industry-specific solutions emerge in banking, government, insurance and healthcare: With increased regulatory environments requiring API management, some API management service providers are creating accelerators and specific offerings to meet industry specific needs.

- API Security is now a standalone product. Privacy is the next differentiation maker: There is some blurring of boundaries between API security, access and identity management, API testing and API analytics and metrics. This unbundling and rebundling of security-related features is expected to continue over the coming year as security products extend to meet all possible threat vectors. Regulatory compliance products are expected to follow a similar trajectory in 2022, especially as data management platforms expand as a separate grouping to traditional API management platforms.

- APIs are a new layer of business and tech infrastructure: As data usage and digital infrastructures increase and become the norm, product APIs will become essential infrastructure products utilised by all businesses. We expect to see a growth in both data products being made available via API, but also increased services and functionalities being made available via API.

- Low code and the growth of citizen developers is enabled by APIs: We expect to see a greater range of tools and more API integration platforms over the year ahead as API management solutions and other API tool providers increasingly add low code features so that non-engineering team members can make use of APIs directly.

In my endnote for the report, I discussed how current global trends are evolving the world’s core operational services infrastructures towards digital systems, and that APIs will be essential to enable this infrastructure to support open ecosystems in which all stakeholders can co-create, collaborate, complement each other, compete, and/or coordinate. COVID-19 has also forced the hand of global industry towards enabling connected digital systems to become the norm. I called this “the beginning begins in earnest”: for the past ten years, we have been talking about how APIs are growing, and pointing at cases like Twilio and Stripe to demonstrate this developer-first economy. I have worked with the European Commission to define an API Framework for Digital Governments and with the World Bank on encouraging API infrastructures amongst digital services providers in low and middle income countries in order to spur the development of financially inclusive products and services. With open banking and open finance well under way, open health now a priority to enable health data sharing and optimised use of health resources, and open energy next on the horizon, the world’s core infrastructures have become digital and are able to foster open ecosystems.

What next?

Platformable will be working with apidays throughout 2022 to maintain the API Landscape as an industry-wide resource:

- We will support apidays to keep the data up to date. apidays will share updates on trends with the community at their events throughout 2022. Look out for an update at the first apidays virtual event for 2022, Helsinki and North, being held on March 16 & 17, 2022.

- We will refine the data model and taxonomy. The original categories and sub-categories used to group the API industry need a refresh, given how much the industry itself has moved, and where we expect it to head. For example, data management platforms have sprung up as a whole new category and field, and we are seeing these converge somewhat with API tools. We also have event-driven architectures and IoT infrastructures grouped together, reflecting the industry use cases of several years ago, and again we would like to split this out a bit more. We will also add open API standards, media, and industry associations to our landscape, and we will look at how to expand data items based on industry need. For example, if the API Landscape can be used by digital businesses to help with purchasing decisions and vendor comparisons, we could add data fields that map the features offered by each tool to assist with making informed decisions and comparing tools.

- We will extend the value of the API Landscape. With such a quick project turnaround, we were only able to do limited usability testing when we first launched the landscape tool, but we would like to run some surveys and focus groups with API tool providers and other potential users to see how we can elevate the API Landscape as a go-to industry resource throughout 2022. We will also be launching monthly trends reports with summaries of new investments, employment growth, new feature rollouts and industry partnership arrangements.

- We will update our key themes for the year, and track emerging tech and new standards. Even this month, we are already seeing how the five trends we defined are progressing. Our predictions for the strengthening of the API security market (Trend 3) has already been demonstrated with Noname Security bringing in $USD135 Million in new investment in December 2021, shortly after the release of our report. Our prediction on APIs as a new layer of infrastructure (Trend 4) are demonstrated by news like today’s announcement that the US Department of Veterans Affairs has selected Google’s Apigee platform to help build new tools and enable data exchange via APIs. And our predictions on the importance of new no code platforms (Trend 5) suited to specific industry verticals (Trend 2) are seen in steps forward like the announcement that the low code connector that ISD FENIQS built to integrate directly with Nordigen’s API aggregation platform will be available within the OutSystems app development platform.

How can you be involved?

We would love your support as we build out these resources for the API industry and community. Here are four things you can do to get the most out of the API Landscape Tool and Trends reports:

- Of course, register and attend apidays events throughout 2022, and consider speaking and sharing your expertise with the community

- If you are an API Tools provider, help keep your data up to date

- Anyone in the broader API economy can share feature ideas with us, and let us know how you would like to use the data and trends available through the apidays API Landscape

- Please subscribe for news on our Trends Report releases and to hear about our focus group research to ensure you get value from the API Landscape and analysis. Use the form below:

Mark Boyd

DIRECTORmark@platformable.com